How To Find Out How Much Money Is In Your Federal Reserve

The Federal Reserve's monetary policy has stabilized the Usa fiscal system, but its power to assist the economy recover more than swiftly is more limited than many people may exist willing to take.

"We lent by every means possible and in modes we had never adopted before."—Jeremiah Harman, director of the Bank of England, argument before the Bank Lease Committee on the depository financial institution'south policy during the Panic of 1825.ane

In the past 12 years, the U.s.a. Federal Reserve (the "Fed") has faced 2 major fiscal crises. One started inside financial markets (the housing finance plummet of 2007–2009) and one involved an outside shock (the COVID-xix pandemic). The Fed responded in each case with an alphabet soup of new programs, and despite the differences between the ii crises, these actions had a like result: stabilizing the financial organisation. Simply in both cases, the Fed'south bear on on employment and economic growth has seemed sluggish at all-time.

If the Fed tin shore up a tottering fiscal organization through monetary policy, why hasn't it been able to help the economy recover more than swiftly? The candid reply is that the Fed's power is more express than many people may exist willing to accept. In both the 2007–2009 and the 2022 crises, the Fed pulled many levers in its endeavor to avert total fiscal organisation collapse, but these levers focused on keeping the financial arrangement operating. That'due south a necessary—but not sufficient—requirement for a healthy economy. If businesses continue to see excess capacity, and if consumers are worried about the futurity and unwilling to spend, the economy volition suffer—and there is piffling the Fed can do. Specially today, when interest rates are already at nearly-zippo levels, the Fed just doesn't have the tools to put the economy back on track. To speed the recovery, the onus should be on Congress and the president—non the Fed—to consider how best to get the economic system moving again.

Why does the Fed be?

To sympathise why the Fed'south leaders took the actions that they did in 2022—and why those actions are having an important, but limited, impact—it helps to know something about the Fed's purpose.

The financial system appears at get-go glance to be very technical. Only it's not really that complicated. The financial arrangement—banks, stock markets, financial planners, traders, hedge funds—exists to match savers (generally households) with people and organizations (investors)2 who wish to turn those savings into capital letter assets—buildings, machines, even ideas—that produce goods and services. The players in the arrangement—"financial intermediaries" in the jargon of finance—offer a broad variety of "products" designed to balance the needs and desires of the savers with those of these savings' users (the aforementioned investors). These investors are mainly businesses that wish to increase their capacity to produce goods and services by purchasing uppercase goods such every bit buildings and machines. Financial products that help to connect savers and investors range from savings accounts at banks to exotic derivatives.

Many financial products are traded in markets, which allows savers to purchase and sell buying of those assets as they see fit. If there is regular trading in a market, financial experts say that information technology is "liquid." Savers similar assets that are traded in liquid markets because they tin can sell them any time they wish. Investors like liquid markets because they can program on being able to borrow when they demand greenbacks for operations or even just to make payrolls. Merely what happens when trading stops in a liquid marketplace?

That'southward not an academic question. Information technology is precisely what happened on a regular ground starting in the early 19th century as the number of financial products multiplied. These financial "panics" occurred when people suddenly decided that they didn't want to hold a particular asset, and trading in that asset suddenly stopped. Suddenly, fiscal intermediaries could no longer match savers and investors. The result: The economy's ability to back up investment—houses, commercial buildings, industrial machinery, computers—plunged because those wishing to acquire capital goods found it incommunicable to find financing. When this happens, the economy goes into a tailspin. The same pattern has held from before the British Railway Mania of the 1840s through the global fiscal crunch of 2008–2009.

One of the Fed'due south fundamental responsibilities is to prevent such panics, or at least to forbid them from having a large affect on the real economy of production and employment. The simplest way to practise this is to provide money—liquid assets—so that savers and financial intermediaries tin can see their obligations. Only in addition, the Fed and other central banks can footstep in to continue markets functioning. That's what the Bank of England did in the early 19th century—and that's what the Fed has been doing in 2022. The quote at the showtime of this article comes from a parliamentary investigation of the Panic of 1825, and describes the Fed'south actions this yr remarkably well.3

The pandemic panic

US fiscal markets started to react to the spread of COVID-19 in early March. The pandemic created a huge amount of uncertainty, impelling traders to go unwilling to trade anything that might be at take chances from the pandemic. This led to a sell-off in markets that were perceived equally being risky and a strong want to hold the safest assets possible—US Treasuries. Without asset buyers, some markets looked similar they might shut downwards completely.

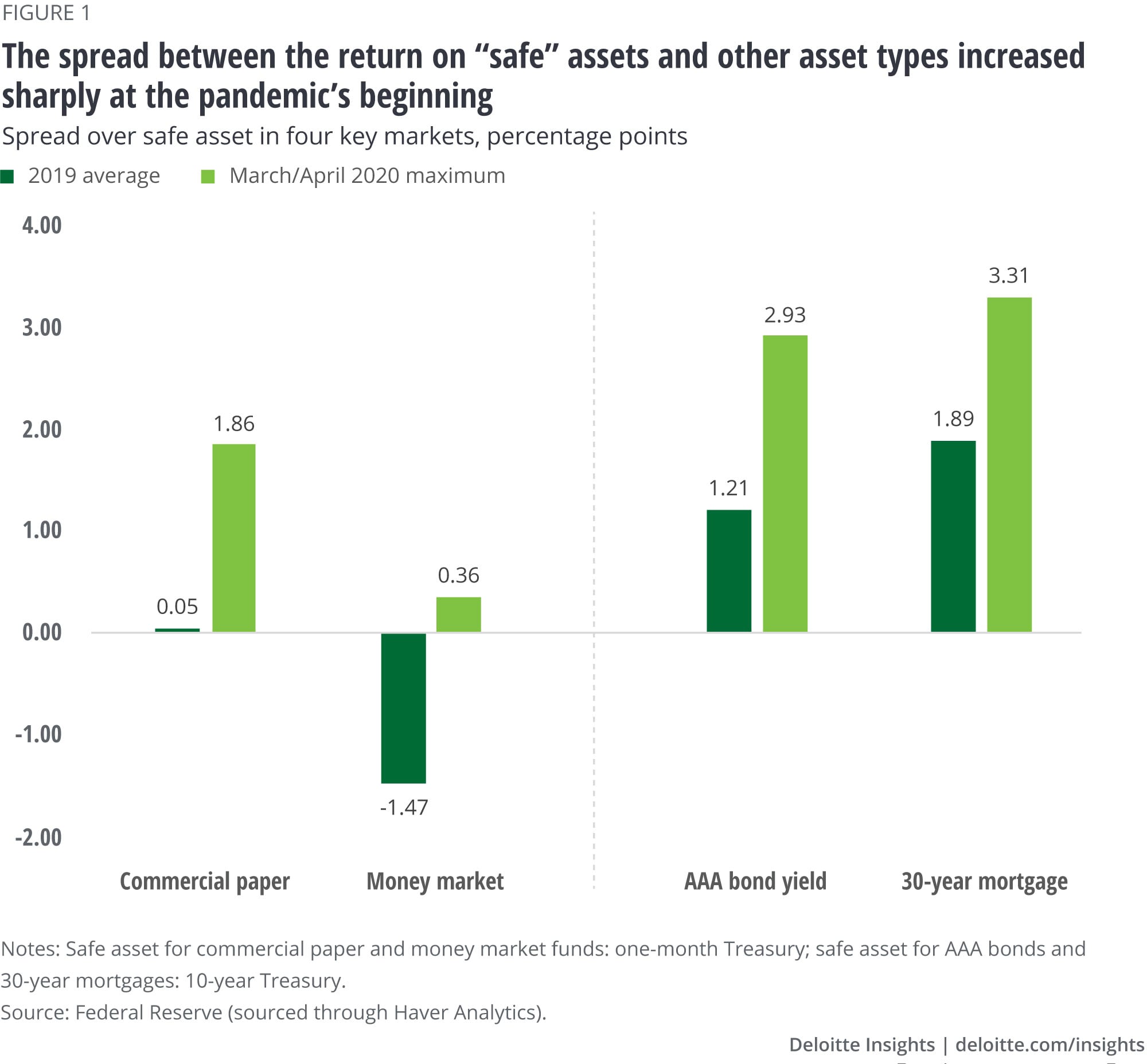

This was evident in the returns being offered to savers to entice them to buy those assets. Figure 1 shows the spread, or percent point departure, betwixt the return paid in 4 central fiscal markets compared to the return on a "prophylactic" asset (a Treasury security of like duration). The boilerplate spreads in 2022 are a expert measure of "normal" spreads that account for the (sometimes slight) differences in the overall riskiness of these assets. For case, commercial paper is a shut substitute for Treasury bills, and near every bit rubber. Under normal weather condition, the spread between them is very small. Simply in March 2022, the involvement rate for commercial newspaper suddenly soared above the charge per unit for Treasury bills, for a spread of most ii%. This reflected a sudden preference for Treasury bills by savers seeking safe short-term places to park their money. For businesses that depended on commercial paper markets to obtain cash, the higher involvement rate was a sudden and unexpected cost. Worse, there was the possibility that savers, thinking that private debt would be too risky, would simply shun the commercial newspaper market at any interest rate. If that were to happen, it would leave businesses that planned to raise coin via the commercial paper market brusque of cash, and mayhap unable to pay bills or salaries that depended on that cash.

Something like happened in other markets. For instance, short-term money markets of a sudden became suspect relative to the safety and liquidity of short-term Treasuries. Corporate AAA bonds also suddenly looked risky, and the markets forced up the yield relative to equivalent long-term Treasuries. And many savers did non desire to take on the boosted risk of holding mortgages in an economic system with high unemployment, so the mortgage charge per unit spiked relative to Treasuries. Considering of these developments, corporations using the bail market to fund investments and homebuyers wanting to purchase a house might have found the market dried up and their plans interrupted.

That's why the Fed stepped in. First, it did something very traditional: It supplied a lot of liquidity in the course of cash and then banks could intervene if necessary. But that wasn't actually enough. So the Fed then became a straight buyer in a multifariousness of financial markets to be sure that those markets could continue to operate. This prevented businesses and households that had planned to apply those markets from having their access to greenbacks interrupted.

Each market required a separate programme, so Fed watchers were inundated with alphabet soup: the MMLF (coin market place liquidity facility), CPFF (commercial newspaper liquidity facility), MSLP (primary street lending program, to purchase loans extended to smaller businesses), MLF (municipal liquidity facility, to buy short-term state and local debt). Each plan has distinct requirements and limits tailored to the marketplace the Fed wishes to support.4 Some require more Fed activity than others. Just all share the goal of keeping open up a particular channel for connecting savers and investors.

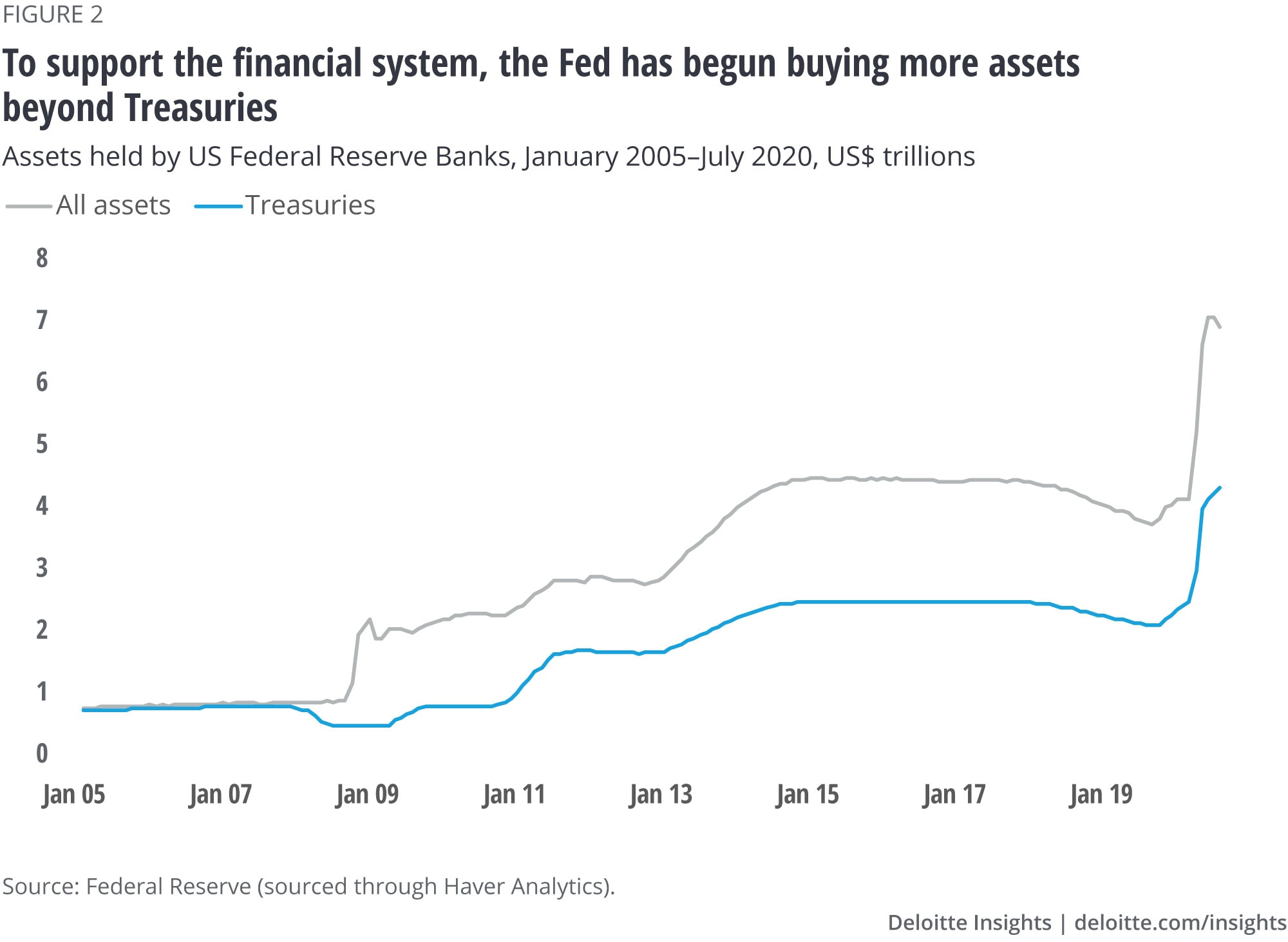

Supplying liquidity, and so buying all those assets, have ballooned the Fed's residuum sheet. Figure ii shows the full avails held by the Fed from 2005 to 2022.

Until the 2007–09 global financial crisis, the Fed held merely Treasuries.5 A key office of the Fed's response to the global financial crisis after 2009 involved purchasing longer-term Treasuries and mortgage-backed securities (MBS). That motion was the famous "quantitative easing," which generated a lot of contend in the mid-2010s. You can see the ascension in assets endemic by the Fed around that time.

In 2022, the Fed started to accept steps to reduce its holdings of MBS and longer-term Treasuries, beginning by non replacing maturing MBS, and and then past actively selling the remaining holdings at a slow, steady stride. That was interrupted past the pandemic, still, and the Fed is at present ownership (and sometimes selling) a surprising diverseness of avails. At the finish of July 2022, the Fed held U.s.$2.vi trillion in non-Treasury assets, nigh 37% of its balance sheet. And financial markets continued to operate normally. The Fed's actions successfully prevented the pandemic from causing a financial crisis—no small feat.

What? No aggrandizement?

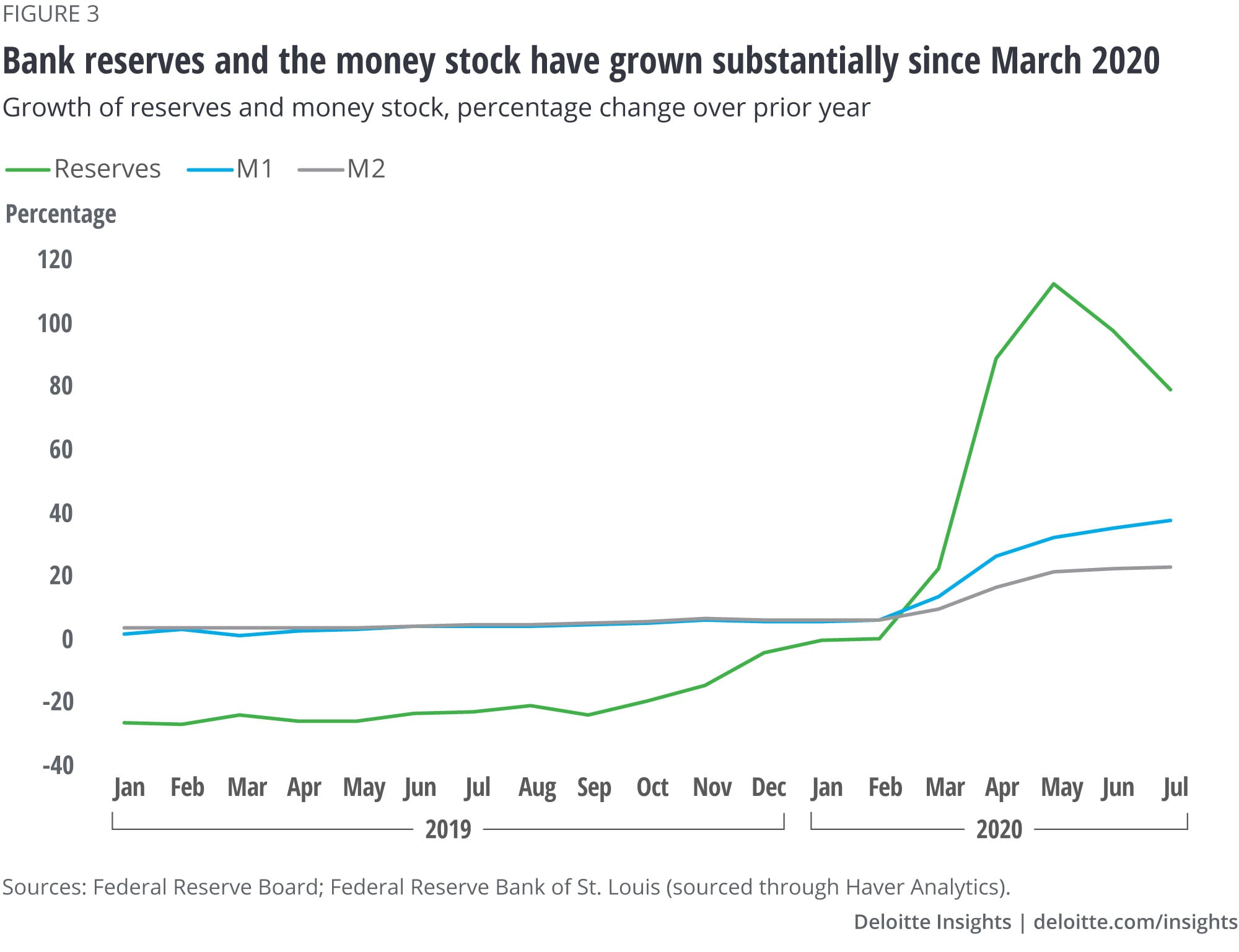

As whatever auditor knows, a balance sheet balances—which ways that the Fed'south liabilities grew with its avails. The liabilities of a central bank are mostly currency and commercial banks' reserve deposits. Banks are required to concord reserves, with the amount depending on the size of the depository financial institution deposits (such every bit checking accounts) they have outstanding. Because bank deposits are the main form of money in a modern economic system, the Fed's creations of reserves should—under normal circumstances—determine the size and growth of the money stock.

Sure enough, as figure 3 shows, March 2022 saw a sudden acceleration in bank reserves in the two most common measures of the money stock: M1 (currency and checking accounts) and M2 (M1 plus some savings and fourth dimension deposits). With M2, the broadest measure out of money, growing at over twenty% in the past twelvemonth, tin inflation be far backside?

That conclusion is a severe oversimplification of bones budgetary theory. According to the theory, inflation is described past an equation that many readers will remember having learned in an economics class:

MV = PT

1000 is the supply of money, V the velocity at which coin circulates (i.eastward., the number of times in a given catamenia coin is used, on average), and PT the value (price times number) of total transactions in a given time. If the velocity and the number of transactions don't modify much, a large increase in Grand, the supply of money, should create a large increase in P, the price level. And if the money supply grows speedily, the price level will follow—pregnant the economy will experience inflation.

As is often the example in economics, nevertheless, it's the assumptions that matter. The velocity of money is not abiding: It depends on how much money people want to concord at any given fourth dimension. And financial crises create weather condition that make people want to hold a lot more than money in their portfolios. This means that velocity, V in the to a higher place equation, has fallen considerably during the pandemic. The velocity of M1, for example, barbarous from 5.five in Feb to iii.ix in March6—reflecting savers' blitz to safer assets and the consequent huge demand for liquidity that threatened to freeze many financial markets.

Because the velocity of coin decreased then sharply (and remains depression), the Fed'southward asset purchases are very unlikely to create inflation even though the coin supply has swelled. In fact, the Fed did the aforementioned thing in 2008, and predictions of future hyperinflation at the fourth dimension proved to be unfounded.7 The median forecast for inflation in 2022 is around two.0%, which means that aggrandizement is rightly very low on the Fed'southward list of concerns. (Run across "Appendix: Who'southward afraid of the big, bad money supply?," for an explanation of the historical context of the argument that coin creation will pb to inflation.)

The Fed'due south new clothes: A change in its stance on inflation

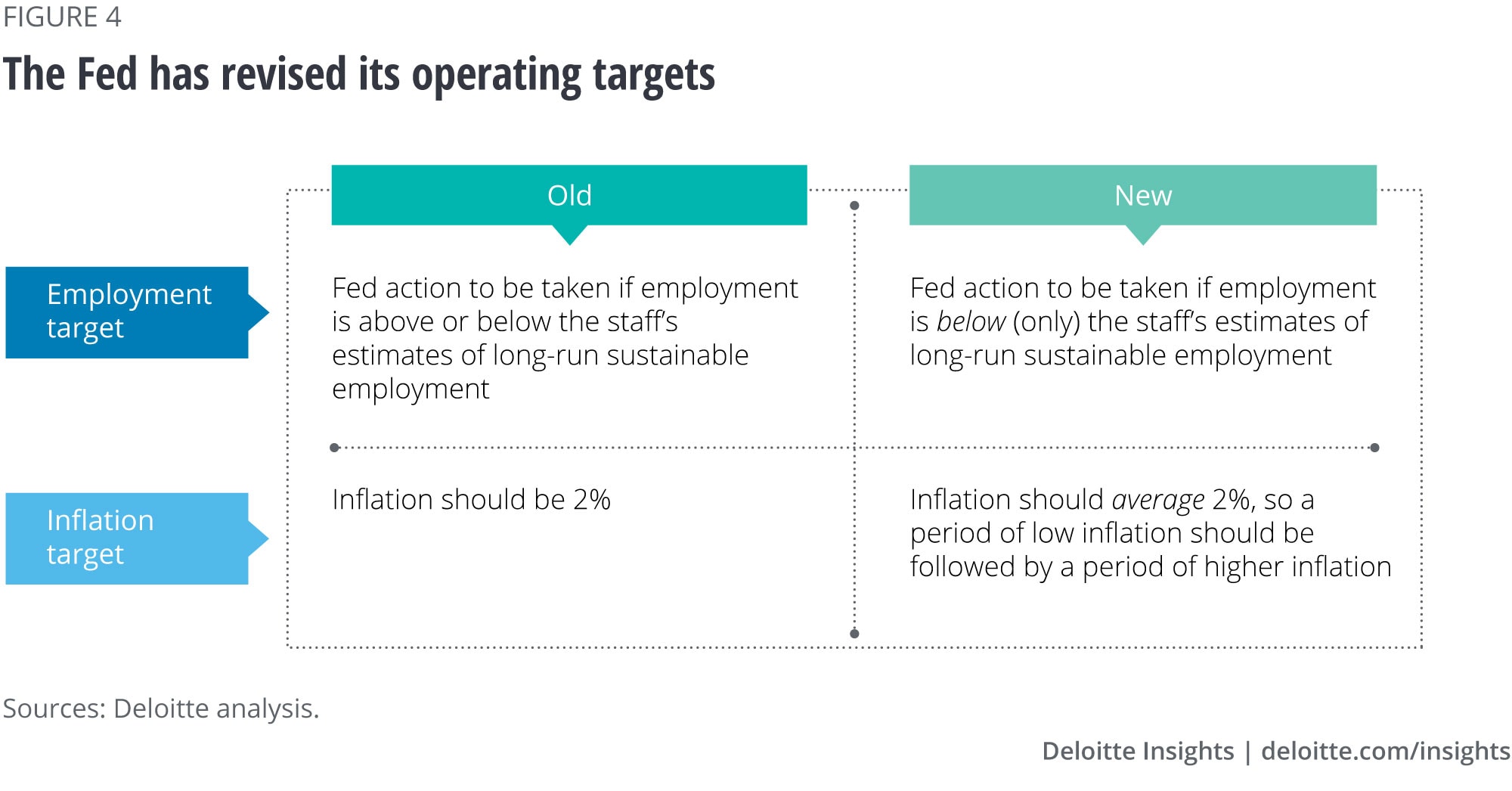

In August 2022, the Fed'due south board of governors announced several changes in how it conducts budgetary policy. Ii primal related changes accept to do with how the Fed defines its inflation target (figure 4). Together, these changes amount to a meaning dovish swing in monetary policy.

The change in the employment target amounts to a very pregnant tweak to the "Phillips curve" concept that economists have used for decades to explain inflation. The Phillips bend continued accelerating aggrandizement to tight labor markets, and so monetary policymakers concerned about aggrandizement looked to proceed labor markets from beingness too tight. At present, in adjusting the employment target, the Fed has declared that it won't exist worried about tight labor markets. It might fifty-fifty welcome them, since it will now effort to push inflation higher afterwards a menstruum of inflation below 2%. This move reflects the experience of the last two recoveries when supposedly tight labor markets never led to college inflation, information technology took very low unemployment rates to induce employers to offer higher wages, and the profit share of national income reached about-record levels.

The modify in the inflation target shows how much the (monetary) world has inverse since the Bang-up Aggrandizement of the 1970s. That episode left economists wondering how to prevent inflation from accelerating. Subsequently trying, and rejecting, a multifariousness of monetary policy targets, cardinal banks hit on inflation targeting as a method of disarming the public that inflation would remain nether control.

What the Fed can't do

As if keeping financial markets operating isn't enough, the Fed is legally required to promote price stability and full employment—the Fed's "dual mandate."eight Promoting price stability has not been a trouble recently: If anything, Fed officials accept been concerned near inflation being besides depression. But the Fed's ability to do annihilation about the current high unemployment charge per unit is very limited, for two reasons.

First, the economy is beingness suppressed by a pandemic, and economic action—and employment—is expected to remain low as long equally people are concerned that economic activity might make them ill. Fed chair Jerome Powell has pointedly said that "the path frontward for the economy is extraordinarily uncertain and will depend in large function on our success in keeping the virus in check."ix The Fed is a powerful authorities bureau, only success in defeating the virus depends on other agencies such as the Centers for Illness Control and Prevention and the National Institutes of Wellness, as well on pharmaceutical companies and the medical profession.

2d, much of the Fed'southward ability to stimulate the economic system depends on its power to manage the supply of credit by manipulating interest rates. Brusque-term involvement rates are already at or close to zero, and long-term rates are at tape lows. The cost of capital was remarkably inexpensive even before the pandemic, but interest-sensitive sectors of the economy weren't responding very much. There'south not much more that the Fed tin can practice to brand the cost of uppercase cheaper, and cheaper capital isn't likely to induce much more spending anyway.10

With the Fed's main tool for stimulating the economy—interest rates—virtually useless right now, the problem becomes one of how to assist the economy recover without it. Just there is a solution. Under current weather, fiscal policy—regime deficit spending—is likely to be a very powerful tool for stimulating the economic system. Later all, with involvement rates likely to stay at record lows, more federal borrowing is not going to affect investment spending past raising the cost of capital. That means that government spending financed by borrowing is likely to be especially effective, since information technology won't exist get-go past lower investment spending.

The lesser line: To help cushion the crisis'due south impact, the Fed has washed its chore and done it well. At present it'south upwards to the rest of the regime to act to support the The states economy.

Appendix

Who's afraid of the big, bad, money supply?

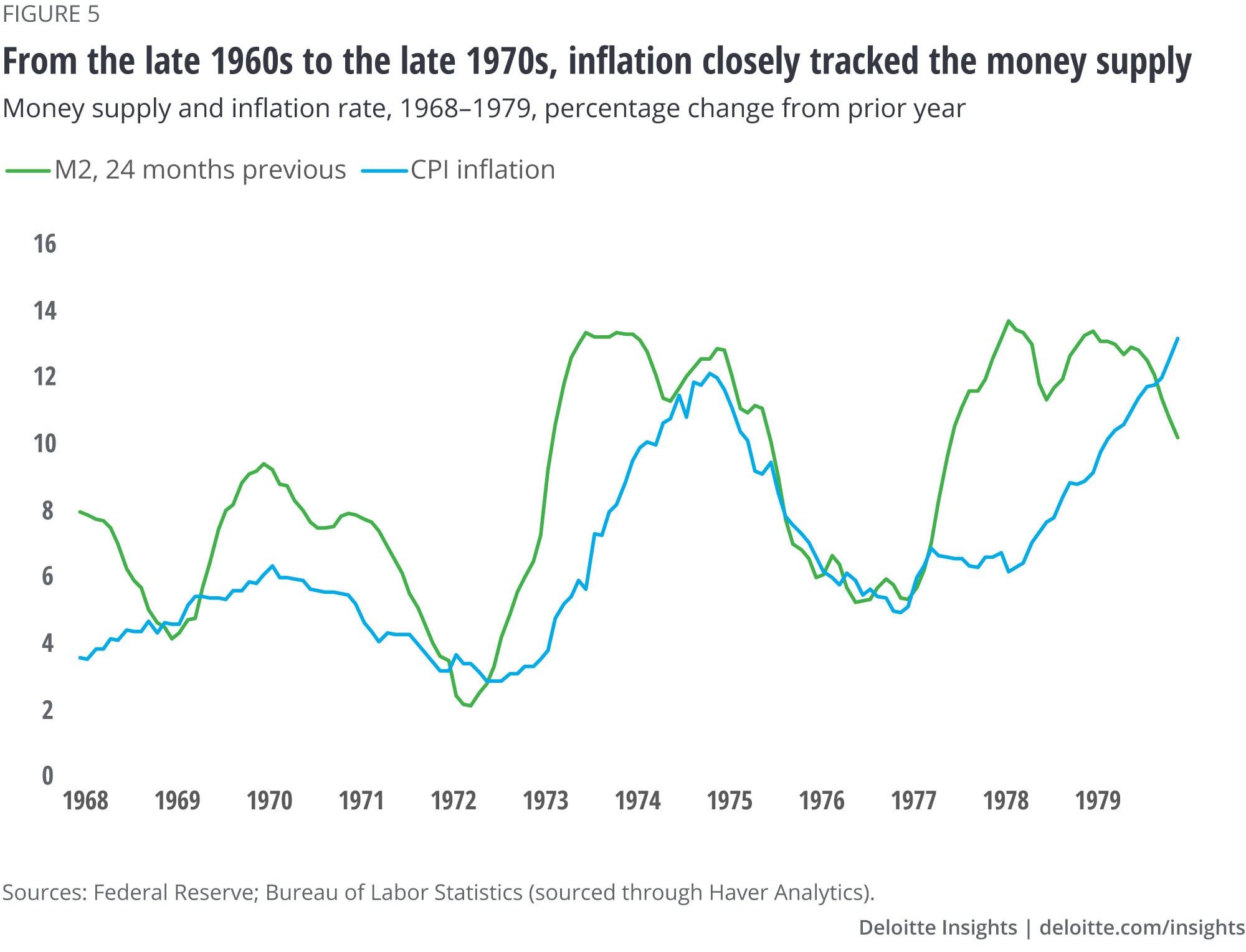

Anybody who learned economics in the 1970s or 1980s—or who read the Wall Street Periodical's editorial page during that menstruum—will accept seen a version of effigy 5. That effigy showed the rate of inflation compared to the growth of the money supply (M2 in this case) from two years prior. The figure'south message was pretty impressive. The best explanation for inflation was past growth in the coin supply—not, as the then-popular view would have it, oil shocks, labor unions, or excessive federal spending. The famous economist Milton Friedman, in whose columns the figure regularly appeared, said that "inflation is ever and everywhere a monetary phenomenon"eleven—fighting words when many economists were focused on other things.

According to Friedman'southward view, the United States will feel very significant inflation in 2022. The narrow money supply (M1) is upwardly 34% over the past year, and the broad money supply (M2) is upwards 23%. Friedman's chart suggests that inflation volition rise to double-digit levels within two years. Nevertheless few if whatsoever economists today are concerned about aggrandizement. Why? And what does that hateful for the consequences of the Fed'south recent actions? The answer to both questions is rooted in the observation that, since the early 1980s, inflation has not tracked the money supply.

Right until information technology was wrong

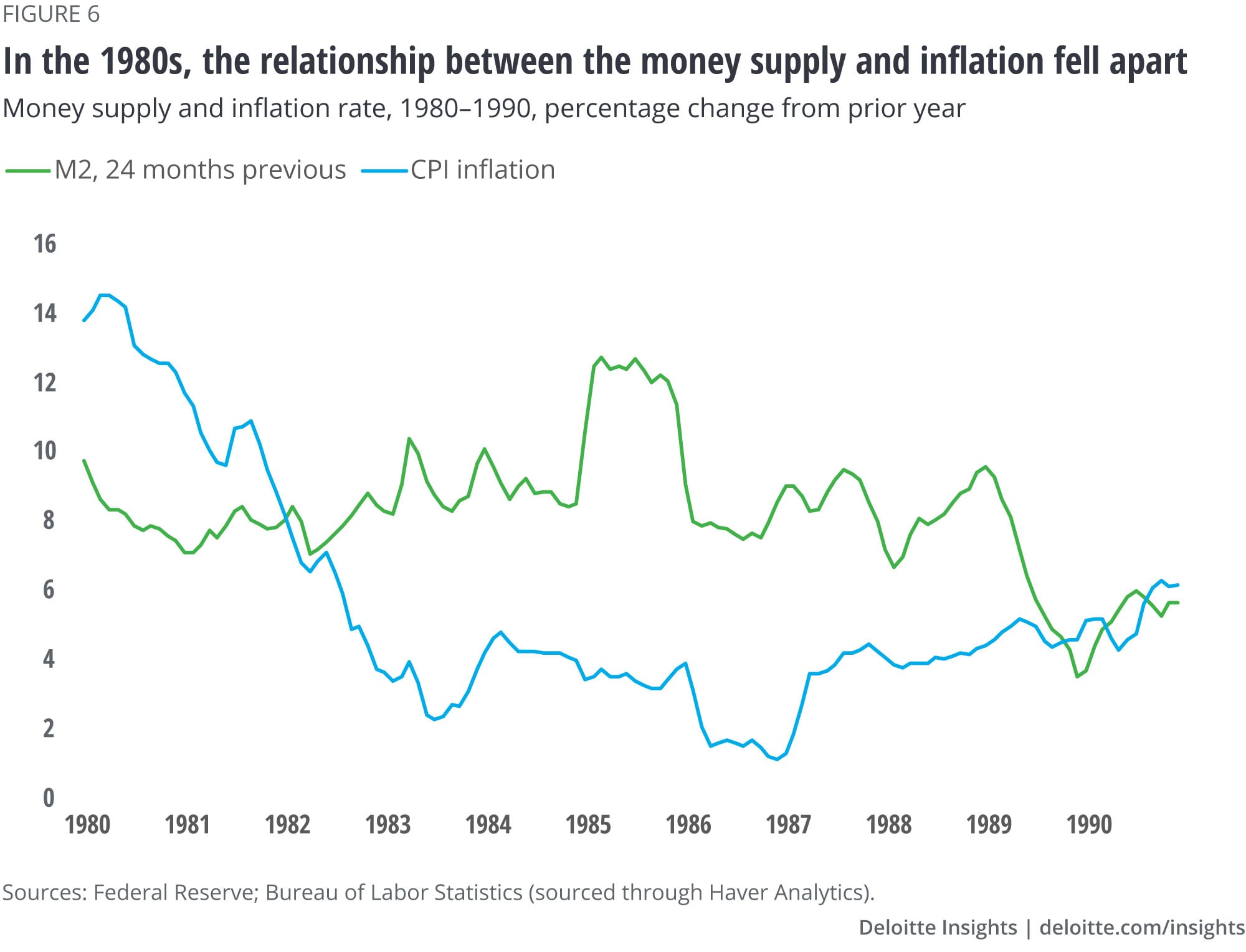

By the 1980s, Friedman's dictum had become more accepted in the economics profession. In fact, the Fed experimented with targeting the money supply to control aggrandizement in the early 1980s. It seemed like a dandy way to get a consistently low and stable inflation rate: Simply brand sure to proceed the money supply's rate of growth low and stable! Unfortunately for this approach, a couple of years into the decade, the relationship between the money supply and inflation roughshod apart. Effigy half-dozen shows the same metrics as figure 5, but for the 1980s.

Despite a steady growth of the money supply in the tardily 1970s and early 1980s, the inflation rate savage. And a spike in the coin supply in 1983 had no impact on inflation in 1985. Instead, inflation savage because of low oil prices.

What is money?

The reason for the collapse of the relationship betwixt money and aggrandizement was quite obvious, even at the fourth dimension. Money every bit a concept must be measured by existing assets in a specific institutional and legal framework. The 1980s saw a period of innovation in assets and a changing legal framework as financial deregulation unfolded. The concept of "money"—assets that can easily be exchanged for goods and services—encompassed a larger and different diversity of bodily assets, and the connectedness between money, every bit measured past the M1, M2, and M3 concepts on the one manus and inflation on the other hand, was broken.

The Fed quickly abased its money targeting efforts, but Friedmanites continued to fence into the 1990s that with just the right measure out, or but by waiting, the magic of figure v would reassert itself, and that monetary policy would in one case again benefit from targeting the quantity of coin. Over time, however, those arguments faded, and the Fed'southward basic operating procedure of targeting price (the easily observed federal funds charge per unit) rather than the quantity of money (whatever information technology might be) became broadly accepted. The Fed'due south recent adoption of new goals (encounter sidebar, "The Fed'due south new dress: A change in its stance on inflation") takes it even further from the "monetarist" view that Friedman popularized in the 1970s.

Source: https://www2.deloitte.com/us/en/insights/economy/issues-by-the-numbers/federal-reserve-monetary-policy.html

Posted by: estellhosess.blogspot.com

0 Response to "How To Find Out How Much Money Is In Your Federal Reserve"

Post a Comment